[Part 1] The market correction is unlocking bargains. Here's what's on my list and why

Quality stocks on sale, earning growers, a few thematic plays, and turnarounds at even deeper discounts.

I haven’t seen a more entertaining politician than Mr. Trump. From threats of taking over Greenland & Canada, levying reciprocal tariffs, withdrawing from the Paris accords, rise and crash of Trump coin, intimidating Zelensky, rebuking spending policies under DOGE; the list goes on and on. All of that and then you realize it has been less than two months since his reappointment.

It’s an understatement to say that the current correction is partly induced by the new administration. Honestly though, it was a long time coming. The market was just a nudge away and Trump’s antics was that much awaited trigger for the sell-off.

I don’t know how deep the current drawdown will be but I have a notion of where we might be getting around.

A further 4-5% price correction in the coming month followed by 3-6 months of lull where the broader market will be flattish and consolidate. Recovery this time around would be ‘W’-shaped rather than a ‘V’.

All of this, thus provides us an opportunity to sit back, sip coffee and relax research. In the past year, there would have been stocks that would have had our attention but they were too pricey. Many of them are now available at discounts. They may not be attractive yet but we are getting there.

This is a two part series where I review a bunch of companies in a single post. These are companies I consider great prospects but fall slightly short. Either valuation is not sufficiently cheap, future cash flows reasonably uncertain, or my research on the product isn’t mature enough to predict terminal value. In a nutshell, the risk/reward profile is not quite good enough at the current moment.

However, I am tracking these companies with rigor. Because someday, some random market sell-off could shave off 10-15% which may make these companies attractive for a brief period of time. And at that time, I would rather act than think.

In fact in some of the following companies, I hold a tracking position or a little more. Without further ado, let’s begin:

The Earnings Growers

Shakti Pumps: The company is engaged in the manufacturing of pumps and motors of various kinds which find application in irrigation, domestic, commercial and industrial water supply. The company is a beneficary of the KUSUM scheme and had a net (of GST) order book of ₹1,800 Crs as of Dec’24. The Co has 15 patents to its name and its products are of high quality with ~25% of sales attributed to exports. I wrote about this company in depth a few months back which you can find here.

What’s working for the company:

a) High growth and lush margins: The company witnessed >30% growth in the last two years and management has guided for 25-30% growth y-o-y for the next few years as well. The company was able to hold to an EBITDA margin of ~22% in recent quarters despite increase in prices of modules which is a key component in the manufacturing process.

b) Low debt and high cash: Post its ₹200 Cr QIP in March’24, the company has had reasonable liquidity. Also with a <0.2 debt-to-equity it has a comfortable interest rate coverage ratio of 11.5x.

c) High export traction: The company makes high quality, export grade products. ~40% of the exports are shipped to the US and Middle East and this share is expected to increase. In the export business, management confirmed that margins are higher and receivable periods are lower. The Co has also investing in a new EV subsidiary to produce motors and related parts which will start churning revenues in a year’s time. However, a major chunk of their revenue will still be from the existing business in the near future.

Risks:

a) High working capital: The company’s present revenues are heavily concentrated (~80%) from government projects particularly the KUSUM scheme. As such the Co. suffers from stretched receivables cycle which sometimes extend to almost 6 months. Add to this holding inventory for its 1200+ SKUs. Although, all of this is partially offset via high creditor days, working capital cycles remain a key monitorable for the Co.

b) Constrained order book: Shakti Pumps has a trailing 12 months revenue of almost ₹2500 crores in FY25. If it is to grow at 25% p.a as guided by management, the company has to clock revenues worth ₹3200 crores in FY26. As of date there hasn’t been any significant increase in the order book of ₹1800 crores since its last update as of December. There is a reasonable likelihood that in the near term it may not be able to live upto the growth it has promised.

c) Capacity Constraints and Capital Allocation in DCR cells: The company has a current capacity to produce ₹2500 crores worth of revenue. It is presently in a debottlenecking process of installing machines in its existing facility which would increase the capacity to ₹3200 crores. However, to go beyond the company would need to set up a new plant.

Furthermore, the company is also in the process of a backward integration by setting up a solar cell and PV module manufacturing facility, using wafers as input material. It is also investing in its EV subsidiary to produce electric motors for OEMs. Though, all of it seems ambitious the company might be biting off more than it can chew as these are new ventures by itself. Plus all these would be financed by another round of QIP. Thus equity dilution and capital allocation in these new verticals would be key monitorables.

Garware Hi-Tech Films: The company is an export focused, Indian manufacturer of polyester films and high-margin specialty films. The company’s business is divided into two segments- Consumer Product Division (CPD) and Industrial Product Division (IPD). CPD consists of value added & branded businesses of Solar Control Films (SCF) and Paint Protection Films (PPF).

SCFs are primarily used in vehicles to provide heat & UV resistance for car windows; and are also finding acceptance in architectural segment to provide heat & UV resistance for office spaces and premium real estate segments. Whereas PPFs protect car paint from damages like scratches, dust, dirt etc. These films also have self-healing and hydrophobic properties.

Over last 7 years, Garware has taken some major steps to transform from a commodity business to a value added business. This has led to an surge in sales growth coupled with higher margins. Such that the share of value added business has increased from 48% to 89% and EBITDA margins have increased from 9% to 19% between FY17 and FY24. Also, export share of sales has increased from ~58% to ~78% during the same period.

Garware is a zero-debt company with high cash balance and efficient working capital management. In its effort to backward integrate, the company recently announced the expansion of a new TPU Extrusion Line worth ~118 Crs which is likely to be operational from October FY26.

Risks: All that said, there are some concerns as well. For example, there was debt restructuring done in the past (early 2000’s), the promoters charge a high salary as a % of PAT (FY24: 11.5%, FY23: 17%) and company pays processing charges to a promoter owned entity to the tune of 5-6% of annual revenues. Furthermore, a bulk of its revenue is derived from a sub-segment of the automobile industry which is cyclical in nature. Also, PPFs & SCFs are expensive and are seen as an add-on accessories to car.

For example, I was doing some primary research and found out that a Garware PPF on mass market car like Alto K-10 could cost 50-60k. Hence, for most people buying mass market cars the PPF alone would cost >7-8% of the vehicle’s total cost. PPFs are primarily for premium and high end cars. Many buyers consider substitutes such as Permaguard, ceramic coatings or even better insurance to PPFs.

The stock is currently trading at a PE of 29. I’ll be interested somewhere around 24 given the risk-reward ratio, if I am able to do convincing research.

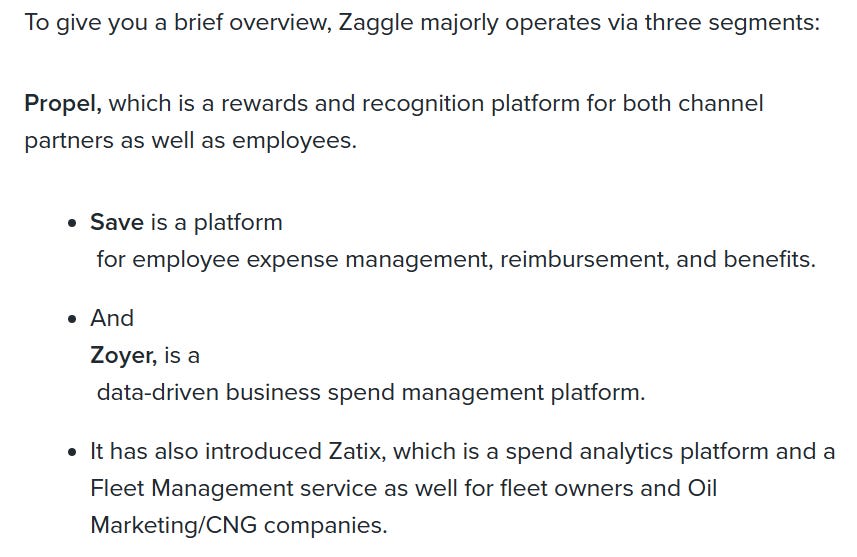

Zaggle Prepaid Ocean Services Ltd: This is a company on which there is a lot of hype and buzz. Marquee investors like Ashish Kacholia and Ajay Kumar Aggarwal have picked up stakes in it. Rightly so, because this is the only profitable listed fintech company in the country. The company has chopped its debt in half via proceeds from its IPO in Sept’23.

The company has corrected 40% from its highs and that has prompted an interest to look into the company closely. However, price correction alone doesn’t turn a frothy valuation into a steal. As Rajeev Thakkar said:

“If the business is not very strong, if the earnings multiple were let’s say 100 times before this fall started and the stock has fallen 20%, then the 100 P/E stock has become 80 P/E. Does that make it cheap? The answer is no. Can it fall further? The answer is yes.”

I have read quite a few articles and coverages on the company and surprisingly no one has taken the time to explain what the company really does. They just put up a generic stuff like:

For a fintech company, it is super important to precisely understand what it does and how it makes money before delving into the financials. I’ll be writing on the company soon. In the meantime, I’ll emphasize you to do your research; my preliminary research has been promising.

The Turnarounds

Paramount Communications (invested 10% of my portfolio): is engaged in manufacturing of Wires and Cables comprising of Power cables, House wires, Optical Fiber Cables & other Telecom Cables, Railway Cables, Specialized Cables, Instrumentation & Data Cables, Fire Survival Cables, etc. It has a strong foothold in the export market (29% of 9M FY25 revenues), with the USA serving as its largest and most prominent export destination.

In late 2007, the company took an audacious gambit by pulling off a debt-funded acquisition of UK based AEI Cables. But for a variety of reasons it didn’t work out and the company’s lenders forced it to restructure. Later in 2016, the debt was taken on by an ARC. During this time, the company went through a period of turmoil and hardship. The business needed cash to grow, the group was still servicing its debts, and there were no ways to raise money. Without working capital funding it struggled to increase business and was compelled to work with few selected clients which gave it favorable credit periods. The promoters had to sell off their personal assets like jewellery, farm houses, provident funds, insurance policies etc. to generate cash.

However, in Aug’24, it prepaid the entire loan of the ARC and became a debt free company. Coming to the present day, I find the Co interesting given the following reasons:

Debt free company - Availing fresh working capital financing from banks can help expand sales and client base

Strong corporate governance with promoter infusion worth 128 crores in the last 15 years including 45 crores in the last 2 years. No shares sold by the promoters; dilution happened during QIP in H2 2024.

Over 30% of its products are exported to the US which shows product strength and acceptance

Current TTM revenue as of FY25 is ~1400 Crs. The Cos long term vision is to cross ₹5000 crores worth of revenue by 2030 and thus acheieve a 30% revenue CAGR. Also aims achieve 40% of the revenues via exports and to improve EBITDA margins by 1%.

Company has been allotted 31 acres of land in MP which will be utilized to establish a green field manufacturing plant.

There are significant tailwinds in the wires industry with little expected impact of tariffs.

As of today it is trading at 1550 worth of Market Cap and optical PE of 16. This is not true as the PE multiple has been considered in a period where tax had been nil for the company owing to offset of past losses.

Adjusting for the tax shield, PE at current prices is 18.6.

At current prices, I am down ~23% on the stock and developing conviction to add more.

SAMHI Hotels: Started in 2010, SAMHI Hotels is India’s third largest owner of hotel rooms operating in 13 cities with 4,800 rooms across 31 hotels. The company follows a business model of acquiring under-managed and under-performing hotels on the cheap and quickly turning them around. Majority of their portfolio (~70% by revenue) is in large office and aviation markets such as Bangalore, Hyderabad and Pune among others. This allows predictable, strong & sustainable growth with less seasonality. The company has a mix of hotels at high-to-mid pricing points and are run by recognized operators such as Mariott and Sheraton.

The company has been consistently posting huge losses (FY24: ₹235 crores, FY23: ₹339 crores) over the past 5 years. Recently in FY25 though, it started turning around profits and has currently clocked a TTM profit of 51 crores. I recently wrote on its turnaround in details here. You can check it out.

Disclaimer: I have stayed and dined in a few of their properties hence I might be biased.

PB Fintech Ltd: India is a hugely coveted credit and insurance market. Huge unbanked population, financialization of savings, underpenetrated insurance markets and all that jazz. PB Fintech via its two platforms PolicyBazar and PaisaBazaar is a play on the same without taking on the underwriting and credit risks.

The platforms sell insurance and personal loans of third party companies and make a commission out of it. Although started as an online company, PB Fintech has been able to build a decent offline presence to target less tech-savvy customers and to build a last mile physical touch points. The costs on brand building and the technology has already been incurred so going forward there’s a high operating leverage at play. Also, onboarded customers have a high lifetime value due to policy renewals in later years where the absolute commission is low but the margins are pure (>85%).

However there are risks. Management rejig early last year where Naveen Kukreja, the cofounder of Paisabazaar and Ashutosh Mishra CFO of Policybazaar stepped down. The company’s priority on growth over profitability and lower adjusted EBITDA margins due to increased investments in building operational capacity (towards the building centers & feet on streets). Also uncertain capital allocation in PB Health (plans to infuse 829 crores) which is yet to begin operations and last year’s foray into the payment aggregator space via PB Pay.

Many have cited a sleuth of corporate governance issues across last year but if you read into it you’ll understand they are immaterial. For example, GST department’s raid in the Co’s subsidiary’s office in Gurugram for alleged tax evasion of about INR 90 Cr. Read further , and you will find similar notices were issued to many other insurance players like Go Digit and HDFC Life for failure to comply with fuzzy GST norms. In another instance, the CEO, Ashish Dahiya was charged over alleged insider trading due to failure to publish a $2M (~₹17 Cr) investment in a Dubai-based marketing company which SEBI identified as ‘price-sensitive information’. Compare that to the Co’s consolidated turnover that year which was ~₹3400 Crs.

In part two of the series I’ll touch upon a few upon a few thematic plays which I am tracking. See you there. Cheers.

Disclaimer: This is NOT an investment advice, just perspectives. My opinions might change anytime and I would not be obliged to update the same here. So please do your own research before making a buy/sell decison.