Garware Hi-Tech Films: Why US Tariffs can be a boon for gaining market share

Issue #7 explores the valuation of an export focused (~50% to US alone) manufacturer of high-margin specialty films in the backdrop of the tariff war and a significant price correction.

As much as this is a blog for curated quality research on small and micro caps, this also serves as our personal investment journal. Writing helps us structure cluttered research and brings clarity in our investment thesis. It helps us to take buy more/sell decisions by comparing what we theorized vs what happened in the future.

Keeping this in mind and in an effort to be more transparent (so that you know our biases) we will begin by stating that:

We hold a high single-digit position in Garware Hi Tech Films Ltd and are looking to add up to ~15% to our portfolio in the coming weeks.

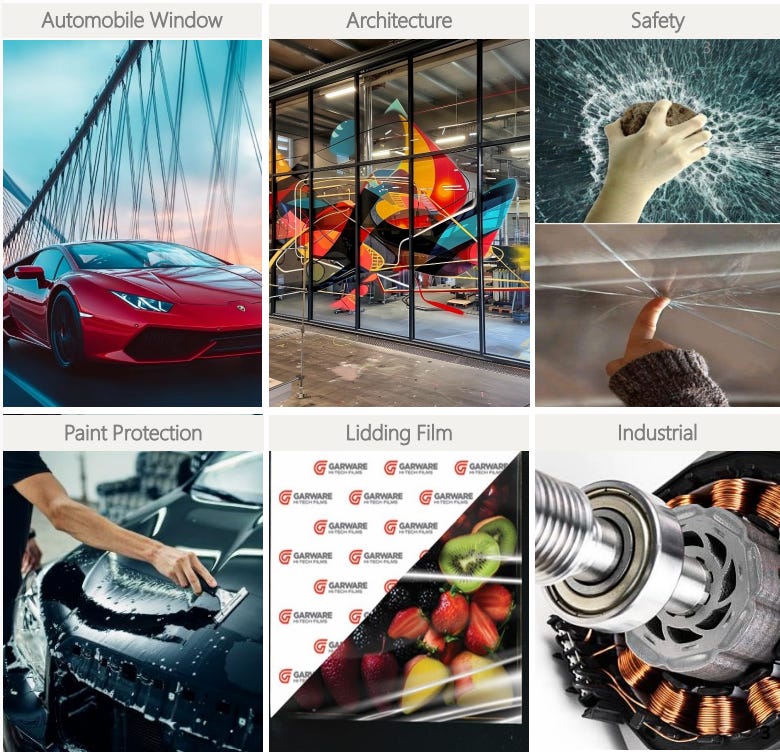

Garware Hi Tech Films Ltd., is an export focused (~50% to US alone) manufacturer of polyester and high-margin specialty films. It’s business is primarily divided into two segments

Consumer Product Division (CPD)

Industrial Product Division (IPD)

The CPD segment consists of value added & branded businesses of Solar Control Films (SCF) and Paint Protection Films (PPF). SCFs are primarily used in vehicles to provide heat & UV resistance for car windows; and also find use in architectural segment to provide heat & UV resistance for office spaces and premium real estate segments. Whereas PPFs are used to protect premium car paints from damages like scratches, dust, dirt etc. These films also have self-healing and hydrophobic properties.

Lastly, the IPD division consists of shrink films, thermal films, lidding films etc. used for everything between packaging F&B, personal care and cosmetics to lamination of book covers, boxes & brochures to EPS insulation for metros, airports and offices.

Over last 7 years, Garware has taken some major steps to transform from a commodity business to a value added business. This has led to an surge in sales growth coupled with higher margins. Such that the share of value added business has increased from 48% to 89% and EBITDA margins have increased from 9% to 19% between FY17 and FY24. Also, export share of sales has increased from ~58% to ~78% during the same period. The company is further integrating via a new TPU Extrusion Line worth ~118 Crs which is likely to be operational from October FY26. This is expected to increase margins in existing products as well as serve as raw material for new products.

Garware is also a zero-debt company with high cash balance (₹572 crs a/o Dec’24) and efficient working capital management (~8 days worth of receivable days!).

All that said, there are concerns as well. For starters, the promoters have historically charged a high salary as a % of PAT (FY24: 11.5%, FY23: 17%); the company pays processing charges to a promoter owned entity to the tune of 5-6% of annual revenues. Then despite having high cash balances, generating healthy free cash flows and no need of intensive capex the company has only distributed ~₹146 Crs of cash in the last 10 years compared to ₹920 crs of PAT & ₹1400 crs of CFO.

Risks in the business side involve that a bulk of the revenues are derived from the premium segment of the automobile industry which is cyclical in nature. Also, PPFs & SCFs are expensive and are seen as an add-on accessories to car.

An excellent, excellent account of all the above and more is documented in great details here by Nirvana Laha. We are not advocates of rephrasing existing research and calling it as our own. We only write on companies or events where we see a gaping hole in curated research.

However, we use peer research extensively for discovering stocks and getting a headway when we begin to study a company. That said, we don’t make any investment w/o doing our own due diligence.

The remainder of the article about is why we believe tariffs can be an advantage to the co & why the current valuations appear attractive to us.

The Thesis

First, PPFs and SCFs are used in premium/luxury cars and real estate. Within this, Garware almost entirely operates in the high-end market where price elasticity of demand is low. These segments are much less cyclical compared to the mass/ mass premium auto-motive and real estate sectors. This is because an increase in prices of goods has way less impact on demand for customers who are extremely wealthy.

Second, an increase in tariffs can actually increase market share for Garware. There are two reasons for this: 1. Garware enjoys a low cost production advantage owing to being the most vertically integrated manufacturer of automotive films in the world. This enables high margins for both Garware and the dealers compared to competitors like 3M, Xpel, Eastman (Lumar). If tariffs are levied, these margins will be squeezed but even more so for competitors who mostly rely on contract manufacturers. They might not have the wriggle room to cut prices (compared to Garware) and will instead pass on the tariff impact to customers. This makes Garware’s goods more attractive in terms of both quality and price.

The below table shows that most competitor sell atleast at a 100% premium to Garware’s brand Global:

India is relatively in the lower-middle segment of Trump’s announced tariff spectrum. Assuming that all PPF brands take the same price hike say 20% as Garware to pass on the tariff impact to their customers; Garware’s product (being lower priced) will see a much small dollar cost increase compared to peers, making them more value-accretive to customers. Eg: 20% increase in a ₹100 product is not the same as 20% increase in a ₹200 product.

Also, as the TPU extrusion line goes live by Oct FY26, the current margins will have a better cushion against price shocks.

Stress-Testing Valuations

Before delving into valuations have a look at the Co’s historical financials:

As of 9th April’25, the Co trades at a market cap of ~₹5600 Crs. With the company on track to clock TTM PAT of ~₹300 Crs imputes a FY25 PE of ~19x. This is cheap both on an absolute and relative basis (given it was trading at double the PE just four months back).

Although we know that tariffs are paused for the next 3 months, assume uncertainty prevails and sales fall off a cliff. Say FY26 revenues take a 30% hit and only amount to ₹1400 Crs (FY25 TTM revenues: ₹2000 crs). Say PAT margins also contract by one-third to 10% (FY25 PAT margins: 15%). That would impute a FY26 PAT of 140 Crs and a consequent FY26 forward PE of 40x. That’s expensive.

However, this does not take into account the ~₹570 crs of cash on the books. Plus, by virtue of its long history, the Co has ended up holding large land parcels in Mumbai, Nashik, and Aurangabad where its plants are located. Most of these land parcels are unutilized right now. The co revalued its land holdings in FY17 causing the book value of land to increase from ₹322 crs to ₹1007 crs due to the revaluation. This is the reason for its depressed ROCE figures, adjusting for which would yield ROCEs over 25% for past years.

We believe the price of this land would have likely increased in this past 8 years. In past concalls, management had indicated they want to sell off the land parcel in Nashik for a estimated realization of ₹100 crs. This would lead to value unlocking by the company and increase investor confidence.

Note the ₹100 crs worth of land parcel is what the co wants to sell; it has other land parcels in the books which it wants to hold. Thus, adjusting for cash & land (₹570 crs + ₹100 crs) we get an adjusted market cap of ₹4800 crs which imputes a FY26 forward PE of ~34x assuming the 30% sales hit scenario. Assuming FY27 revenues revert to FY25 levels of ₹2000 crs and margins partially improve by 200 bps to 12% (FY25 PAT margin: 15%) we get a FY27 forward PE of 24x.

This is a comfortable valuation for a debt free, high cash generating and high ROCE company. Given the current valuations, and likely price corrections in the coming week, we believe the Co would trade at an attractive zone. We hold a tracking position in the stock and would average more in the coming weeks.

Disclaimer: These are my views on the valuation of Garware Hi tech Films Ltd. This is NOT an investment advice, just perspective. My opinions might change anytime and I would not be obliged to update the same here. So please do your own research before making a buy/sell decison.

Hello there,

Huge Respect for your work!

New here. No readers Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing poetic take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

Built to Be Left.

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e